Cisco Systems, Inc. (NASDAQ: CSCO) is popular with investors again. Its shares are up about 19% YTD and up over 50% from a year ago. The S&P 500 has risen almost 10% YTD and is up 20% from a year ago. The moves into security helped, but the trends around artificial intelligence are working in Cisco’s favor.

Now for the big question — is Cisco’s upside played out, or is there more upside to deliver as 2026 comes into focus. Even after an otherwise good earnings report, Wall Street still looks mixed on Cisco for moderate upside ahead after its shares have recovered so much.

While a $70.00 share price is at the top of its $47.85 to $72.55 range over the last 52-week period, Cisco’s shares are still only back close to its old 2000 dot-com era highs if you don’t adjust the price for more than $20 of dividends that have cumulatively been paid since 2011.

Cisco’s current AI target is looking to AI agents to perform daily tasks and to interact with each other. Data centers are also seeing big traffic gains in a way that it boosts the need for Cisco’s optimization and security tools. Those AI agents acting autonomously to conduct tasks along with humans is expected to bring an unprecedented volume of network traffic. It also increases the threat level that Cisco is targeting.

Cisco’s acquisition of Splunk (SPLK) is expected to help Cisco’s customers to prevent security, infrastructure, and application issues from morphing into major incidents. And Cisco noted that, even as some clarity is now seen on tariffs, it is still operating in a complex environment.

WALL STREET CHIMES IN…

No major analyst upgrades have been seen on the heels of Cisco’s earnings report. One common theme, even with those who are less aggressive than Buy/Outperform ratings, is that Cisco’s analyst price targets are still rising.

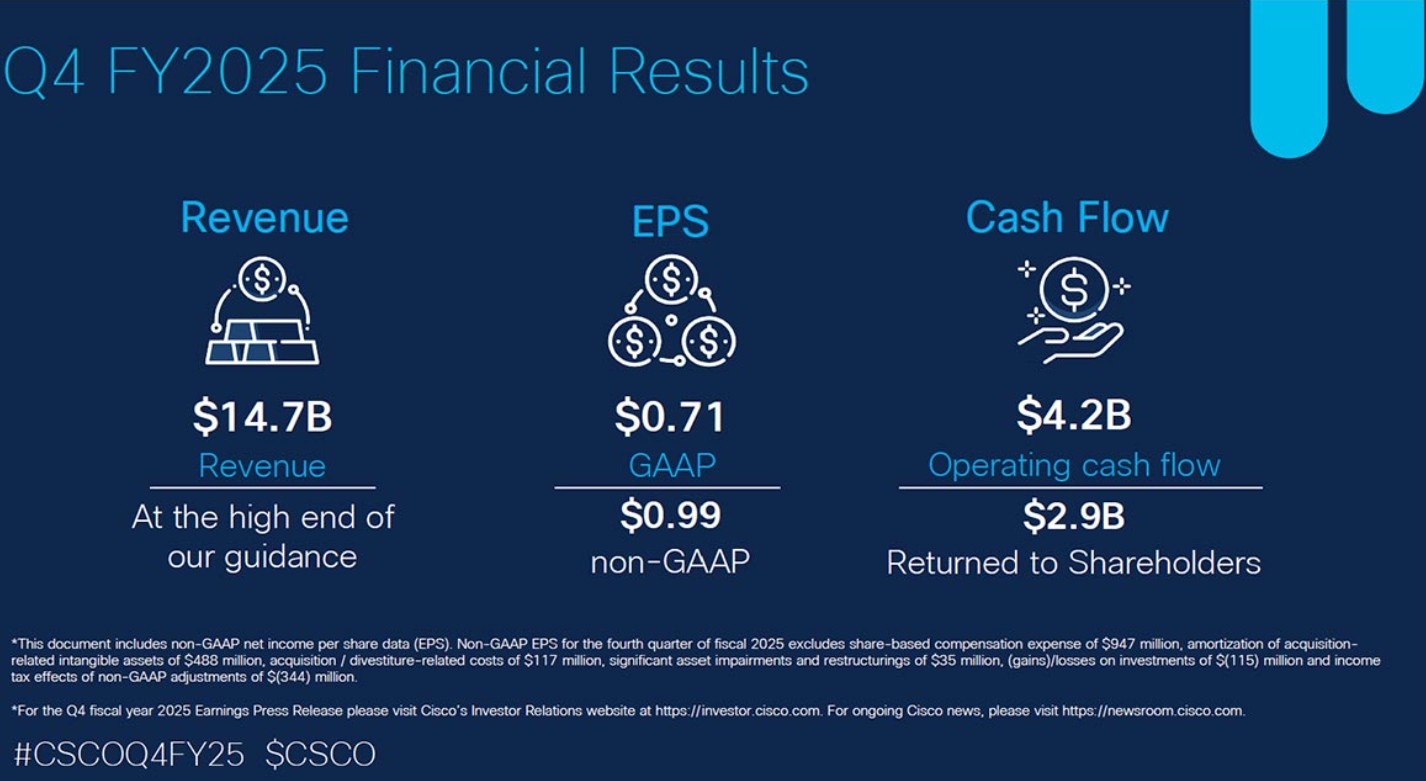

Barclays maintained its Equal Weight rating but raised its target to $71 from $66. The firm noted a slight beat on revenues and earnings and in-line guidance versus consensus. One word that did stand out was that Cisco’s order growth decelerated. That is expected to pose challenging metrics as comparable numbers will be harder to exceed over the coming quarters.

BofA raised Cisco’s price objective to $85 from $76 while reiterating its official Buy rating. And while earnings and guidance seemed to lack “a major spark,” the numbers are deemed to be slightly better than its expectations. The upside is from a revamped portfolio of products and services. BofA also points toward a strong infrastructure cycle around AI and data center growth. Analyst Tal Liani’s Investor Rationale said:

We rate Cisco as a Buy based on our belief that Networking should see renewed growth on normalization of Campus switching demand and Ethernet-based AI buildouts, new product announcements should support growth re-acceleration of its Security business, and we see Splunk synergies supporting growth initiatives in Security and Observability. Additionally, Cisco’s shift to recurring and subscription revenue is positive and helps support the stock, with 50% of revenue now recurring.

Wells Fargo reiterated its Overweight rating and raised its official price target to $83 from $75.

Melius Research reiterated its Buy rating and raised its target to $84 from $78, noting that the firm didn’t expect a new CFO to “get out over his skis” in his first fiscal year.

Citigroup and Rosenblatt both have Buy ratings, with respective price targets now at $80 and $87.

Morgan Stanley still has an Overweight rating, but the firm’s prior target of $70 being raised to $73 is more like an “Equal Weight” rating considering its current share price.

Evercore ISI maintained its In-Line rating and raised its target to $74 from $72 in the call.

UBS maintains a Neutral rating and $74 price target.

CFRA (S&P) has a Hold rating and a $70 price target, noting that Cisco has now become a “show me” story. Still, their report noted how Cisco’s strong balance should allow for further M&A activity, future dividend hikes and continued share buybacks.

Cisco’s balance sheet and forward metrics also look strong. Its cash equivalents was $16.1 billion and deferred revenue was $28.8 billion. It also allocated $1.6 billion in dividends paid and spent $1.3 billion buying back its stock in this last quarter (with another $14.2 billion remaining on its existing buyback plan).

The good news is that Cisco is growing again and with cheap valuations. The bad news is that it is already so large that the current fiscal year (2026) is supposed to see revenue grow 5% to $59.6 billion and then another 5% to $62.6 billion in 2027. Consensus earnings estimates of $4.04 EPS in 2026 (versus $3.81 in 2025) and $4.40 EPS in 2027 keep this stock valued at just 17.5 times expected earnings.

Cisco also should have plenty of room to raise its current annualized dividend payment of $1.64 per share. And its total stock buyback tally is only expected to keep rising.

It would seem that new investors are likely hoping for a pullback in the stock to justify new positions based on its performance and analyst price targets. Those who already hold Cisco look likely to stick with their positions.

DISCLAIMERS

The analyst ratings and price targets mentioned above for Cisco Systems have been credited to each form by name. Tactical Bulls does not have any formal ratings and does not maintain any price targets of its own on the stocks mentioned above.

Investors should keep in mind that analysts sometimes get their thesis and outlook wrong, and market/company fundamentals can change from positive to negative in an instant. Interpretations of how positive or negative the analyst calls are can also wildly vary from investor to investor.

No analyst ratings and price targets, even those with the strongest conviction or strongest pessimism, ever come with any guarantees of profits. Analyst reports also never have money-back guarantees in the event that investors lose money.

Categories: Investing