The stock market may have hit a bump during the first half of November, but most prudent long-term investors should know that the major U.S. equity indexes are still very close to all-time highs. And it is no secret that equity gains seen so far in 2025 have been much stronger than almost all forecasts from the end of 2024. Some investors are wondering if they should lock in gains or whether they should be selectively adding to positions for the long haul.

Goldman Sachs issued a 31-page report this week as a 10-year outlook calling for strong gains to continue in the global equity markets. This may look and feel like a bit of a goldilocks outlook, but keep in mind that Goldman Sachs only caters to high-net-worth individuals and to institutional investors. Even with the high valuations at the present time, Goldman Sachs is forecasting that global stocks are set to rise 7.7% annually over the next 10 years.

This week’s Goldman Sachs outlook was not a prediction that stocks will only go straight up, nor that stocks won’t have any corrections in the coming decade. The outlook excludes large and persistent disruptions like deep recessions or major geopolitical crises. It also does not explicitly model AI productivity or revenue gains. The baseline outlook assumes broadly favorable conditions without incorporating “extreme shocks” or “blue-sky optimism.”

Peter Oppenheimer, the chief global equity strategist of Goldman Sachs Research, sees multiple structural drivers setting the stage for continued stock performance ahead. This includes nominal GDP growth, corporate profitability, and shareholder distributions leading the path for these expected gains. Just keep in mind that this long-term outlook comes with no assurances, and there are no money-back guarantees if these expectations don’t come to fruition.

Oppenheimer’s report does have a caveat about the high valuations today versus what valuations may look like ahead:

Earnings growth remains the primary engine of performance… We expect global earnings — including buybacks — to compound at roughly 6% annually. Dividends are forecast to provide the rest of the return, while Goldman Sachs Research predicts that stock valuations will ease modestly from their current highs.

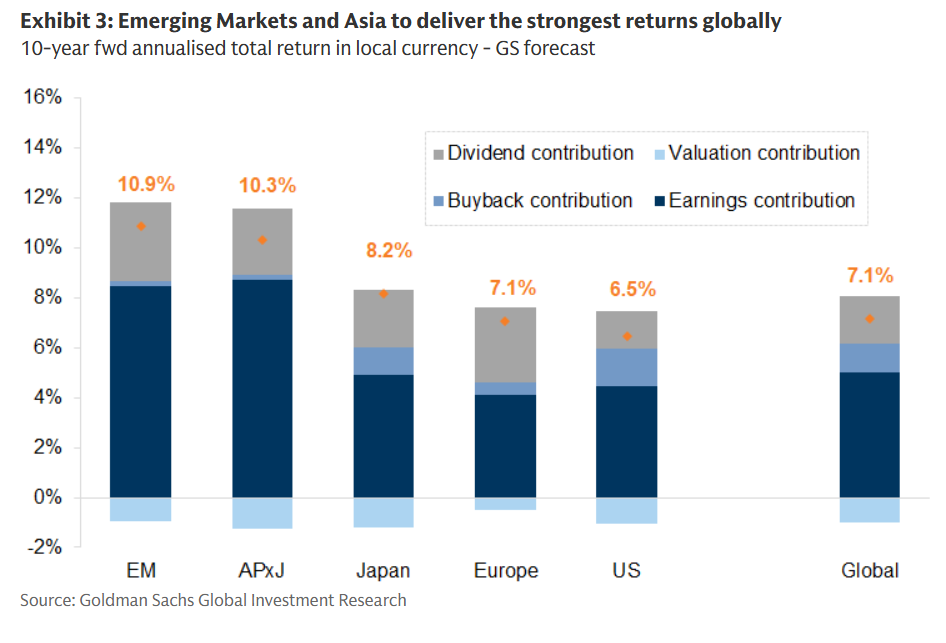

One interesting aspect of this 10-year horizon for tactical investors to consider is that Goldman Sachs isn’t just making the prediction that U.S. stocks are the only (or even the best) place for long-term capital allocations. The 10-year outlook for U.S. equities in 6.5%, but Oppenheimer suggests that investors diversify beyond the U.S. (particularly emerging markets) as a declining U.S. dollar could also favor non-U.S. stocks as an added opportunity. Oppenheimer’s forecast noted:

We expect higher nominal GDP growth and structural reforms to favor emerging markets, while artificial intelligence’s long-term benefits should be broad-based rather than confined to US technology stocks.

The view for the U.S. forecast of 6.5% equity growth on average is driven entirely by earnings and modest dividends, with share buybacks offsetting the present valuation drag. Here are the expected equity growth rates in non-U.S. equity markets:

- Europe at 7.1%, half from earnings and half from shareholder returns

- Japan at 8.2%, with 6% percent earnings growth with a policy-led improvement for payouts

- Asia (ex-Japan) at 10.3%, with ~9% earnings growth and a 2.7% dividend yield, being partly offset by valuation “de-rating”

- Emerging Markets at 10.9%, being led by earnings growth in China and India

The image below shows an actual breakdown by region for contributions from dividends, valuations, buybacks and earnings.

(Sourced from Goldman Sachs)

As always, Tactical Bulls always warns its readers to never use a single investment report or analyst report as the sole reason to buy or sell. Analysts and strategists can get their outlooks wrong just like any investor. Market fundamentals can change in an instant, without warning or updates. And no research report ever comes with assurances or money-back guarantees in the event of losses or if the upside outlook does not come to fruition.