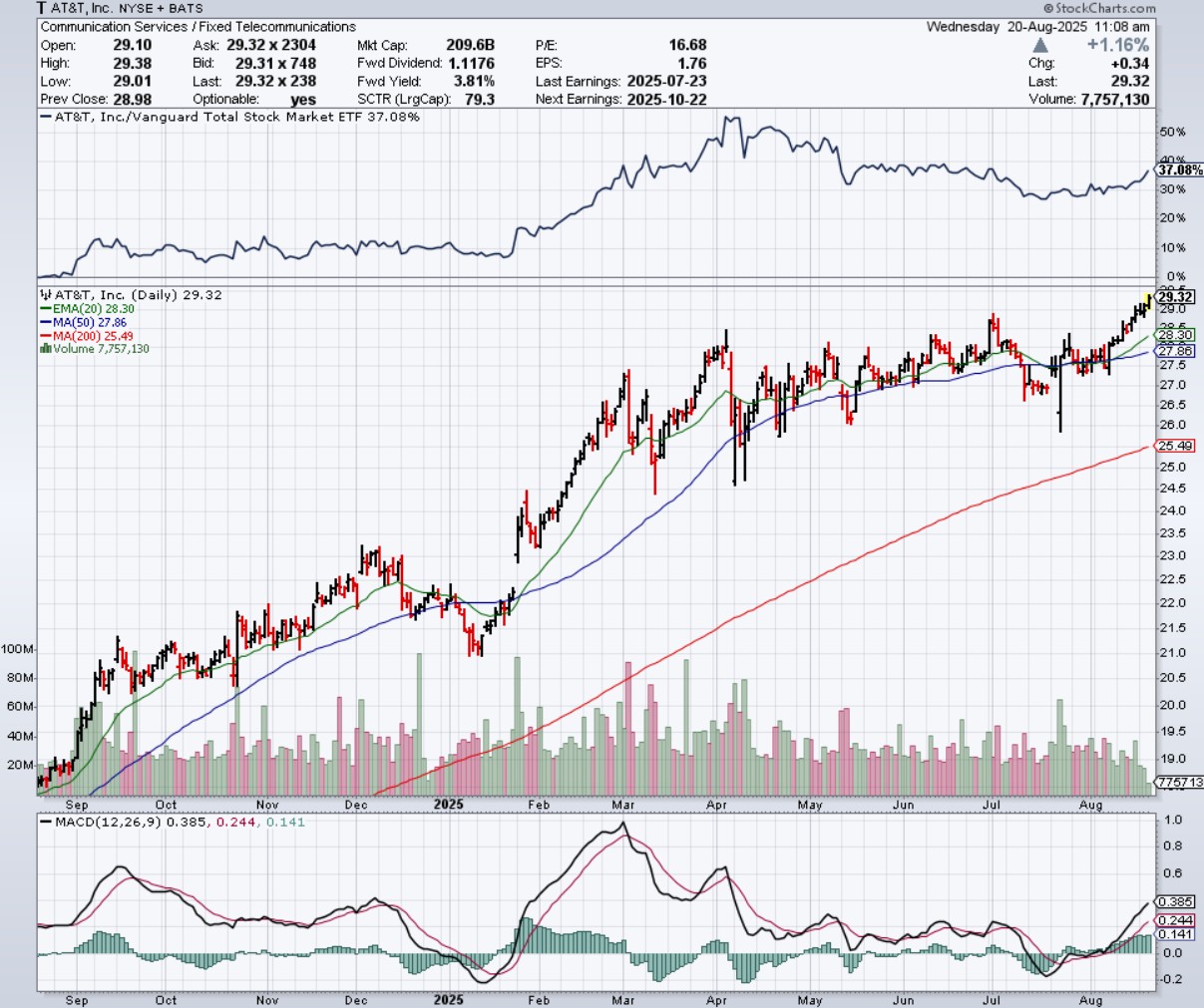

AT&T Inc. (NYSE: T) isn’t usually the most exciting stock to hear about. Well, maybe that’s not true today. The company has been derisking and with shares now above $29 the stock is up over 28% YTD and up 51% from a year ago. Now BofA Securities is adding the stock to its prized US 1 List with much stronger upside potential than its top rivals.

The US 1 List is a collection of “Buy” ratings that are considered its single best investment ideas from each analyst. In short, this is a tactical call with an expectation that AT&T will outperform its peers over the course of the next year or so. If BofA’s Michael Funk is correct, that’s above its old 2016 highs and implies upside of 17% — and that’s before adding in the 4% dividend yield for total return investors.

Tactical Bulls wants to see what this implies for AT&T shares — as well as rivals Verizon and T-Mobile US. Tactical Bulls would also remind its readers that no single analyst call should ever be the sole reason to buy or sell a stock. This analyst call also comes at a time when the “risk-on” stocks have been selling off in favor of many of the defensive stock leaders.

It was just on July 23, 2025 that AT&T’s price objective was raised to $34 from $32 by analyst Michael Funk. He did reiterate his Buy rating at that time, which has been in place for some time. This higher $34 price objective was based on a multiple of 13-times free cash flow estimates (up 14%) for fiscal 2026. Analyst Michael Funk also liked that AT&T is buying back lots of stock and carries a 4% dividend yield. The current consensus analyst price target is closer to $30.50.

BofA’s Investment Rationale:

We view AT&T as fundamentally sound, with a stable subscription-based business model. Historically, the stock has outperformed during periods of M&A and wireless margin expansion-fueled EPS growth and during periods of market uncertainty, when AT&T’s dividend yield and predictable business model have been highly valued.

Verizon Communications, Inc. (NYSE: VZ) is AT&T’s top rival, but BofA rates it only as Neutral. The firm still raised its price objective to $49 from $45 on July 22. That would represent roughly zero-percent upside from the current $45.20 current share price without considering Verizon’s 6% dividend yield. Verizon shares are up 13% YTD and up 11.5% from a year ago.

T-Mobile US (NASDAQ: TMUS) is also rated as Neutral with a $255 price objective by BofA’s Funk. That would represent nearly 1% downside from the current $259 share price, and T-Mobile US has only a 1.2% dividend yield.

Here is how BofA describes its US 1 List in its own exact words:

The US 1 list is intended to represent a collection of our best investment ideas that are drawn from the universe of Buy-rated, US-listed stocks (including ADRs), covered by BofA Global Research fundamental equity research analysts. The list will be managed with a goal of providing superior investment performance over the long term.

There you have it. All opinions and price objectives mentioned above are from BofA Securities. Tactical Bulls has no formal ratings or price targets on any of these top wireless and telecom leaders.

ALSO READ: ANALYSTS DEFENDING RECENT BUSTED IPO

A 1-year stock chart has been provided below courtesy of StockCharts.com.

Chart provided courtesy of StockCharts.com

Categories: Investing