Tactical investors try to look for outsized gains when opportunities present themselves. In the more recent case of Humana, Inc. (NYSE: HUM) seeing a massive stock plunge, there is a scenario brewing that tactical investors may be fighting. Was this a just a huge buying opportunity? Or did this just become the next big short?

Tactical Bulls has been tracking Humana’s stock plunge, as well as the major shift in research coverage in the days since news that the Center for Medicare and Medicaid Services (CMS) cut the quality rating of Humana’s largest Medicare Advantage plan. Here is the problem that has to be resolved — this accounts for roughly 45% of Humana’s Medicare Advantage members. And on top of fundamental research, Humana’s stock chart (see below) was showing significant concern even ahead of the news that crushed its stock.

If Humana’s rating issue is not resolved, this poses a significant potential hit to rebates and quality payments CMS pays Humana in 2026. Until a decision on Humana’s appeal is known, this is a situation where tactical investors may need to consider it a “special situation” rather than an expected outcome based upon set assumptions.

Humana’s earnings and revenues are already in a state of flux and the analyst community already has a wide disparity on earnings and revenues for the coming years. If the more bullish analysts are correct, then Humana is valued at just 12-times forward earnings. If the more cautious analysts are correct, then it’s closer to 14 times earnings. Now imagine what happens if and when those targets have to back out a major portion of revenues from nearly half of the Medicare Advantage members?

Here is where the numbers come into play. Humana’s own 2025 outlook report for 2025 Medicare Advantage Plans already counted over 8.5 million Medicare members as of June 30, 2024; and more than 5.6 million of those members were enrolled in a Medicare Advantage plan.

DISCLAIMER

Tactical Bulls does not have any formal ratings nor does Tactical Bulls issue formal or theoretical price targets for Humana. The ratings and opinions herein are from each listed brokerage firm and the opinions expressed are not the opinions of Tactical Bulls.

WALL STREET SAYS…

Tactical Bulls is taking a synopsis of the disparity in calls here. There have been more than 10 analyst reports showing significantly lower price targets since October 1.

According to Morgan Stanley, Humana’s disclosure lower stars rating was “driven by narrowly missing higher industry cut points on a small number of measures” and that it believes “there may be potential errors in CMS’ calculation of certain of its results and industry threshold cut points.” Morgan Stanley also points out that Humana has already issued appeals to CMS related to the results. The firm also pointed out that Humana expects CMS to release its full results on October 10 and that the company will work on mitigation efforts to 2026 revenue if its appeals are not successful. Its report also points out that Humana noted that its individual Medicare Advantage margin target of at least 3% is now at risk to fully achieve by 2027, and this headwind now pushes out the turnaround story for Humana.

According to BofA’s downgrade to Underperform (Sell equivalent), Humana was cut given the uncertainty of the timing of the margin recovery. BofA now estimates that the loss would be as much as $23 per share headwind in 2026 before any offsets assuming only 50% flows through. BofA noted that Humana is working to regain its ratings and has an appeal pending, but the firm still sees risks that a full recovery might take longer than expected. BofA sees reduced visibility into Humana’s margin recovery and sees a potential for significant pressure in 2026 and beyond due to the loss of Star ratings.

According to Bernstein’s new upgrade (see below), the recent Medicare Advantage star risks are being incorporated into future earnings expectations and into the share price (hence the plunge). This is happening when the sector outlook is improving and at a time when the stock has potential upside catalysts. Bernstein’s view after the plunge is that Humana’s stock is now attractive given the improved operating outlook for Medicare Advantage, reduced uncertainty around the star ratings and repricing execution as some become realized. The reduced stock price now seems to show more upside risks than downside risks. Just keep in mind that Bernstein still lowered its price target on Humana handily despite a formal ratings upgrade.

Here are the research call summaries showing some formal downgrades and almost a unilateral drop in Humana’s price targets:

- Bernstein upgraded Humana to Outperform from Market Perform but cut its price target to $308 from $405.

- BofA downgraded to Underperform from Neutral and target cut to $247 from $376.

- Deutsche Bank (maintained Hold) target cut to $250 from $349.

- Jefferies downgraded to Hold from Buy and target cut to $253 from $419.

- Leerink downgraded to Market Perform from Outperform and target cut to $250 from $400.

- Morgan Stanley (maintained Equal-Weight) target still at $374.

- Oppenheimer (maintained Outperform) and target cut to $280 from $400.

- Piper Sandler downgraded to Neutral from Overweight and target cut to $274 from $392.

- RBC (maintained Outperform) target cut to $265 from $400.

- Stephens & Co. downgraded to Equal-Weight from Overweight and target cut to $250 from $400.

- TD Cowen downgraded to Hold from Buy and target cut to $261 from $402.

- UBS (maintained Neutral) target cut to $250 from $380.

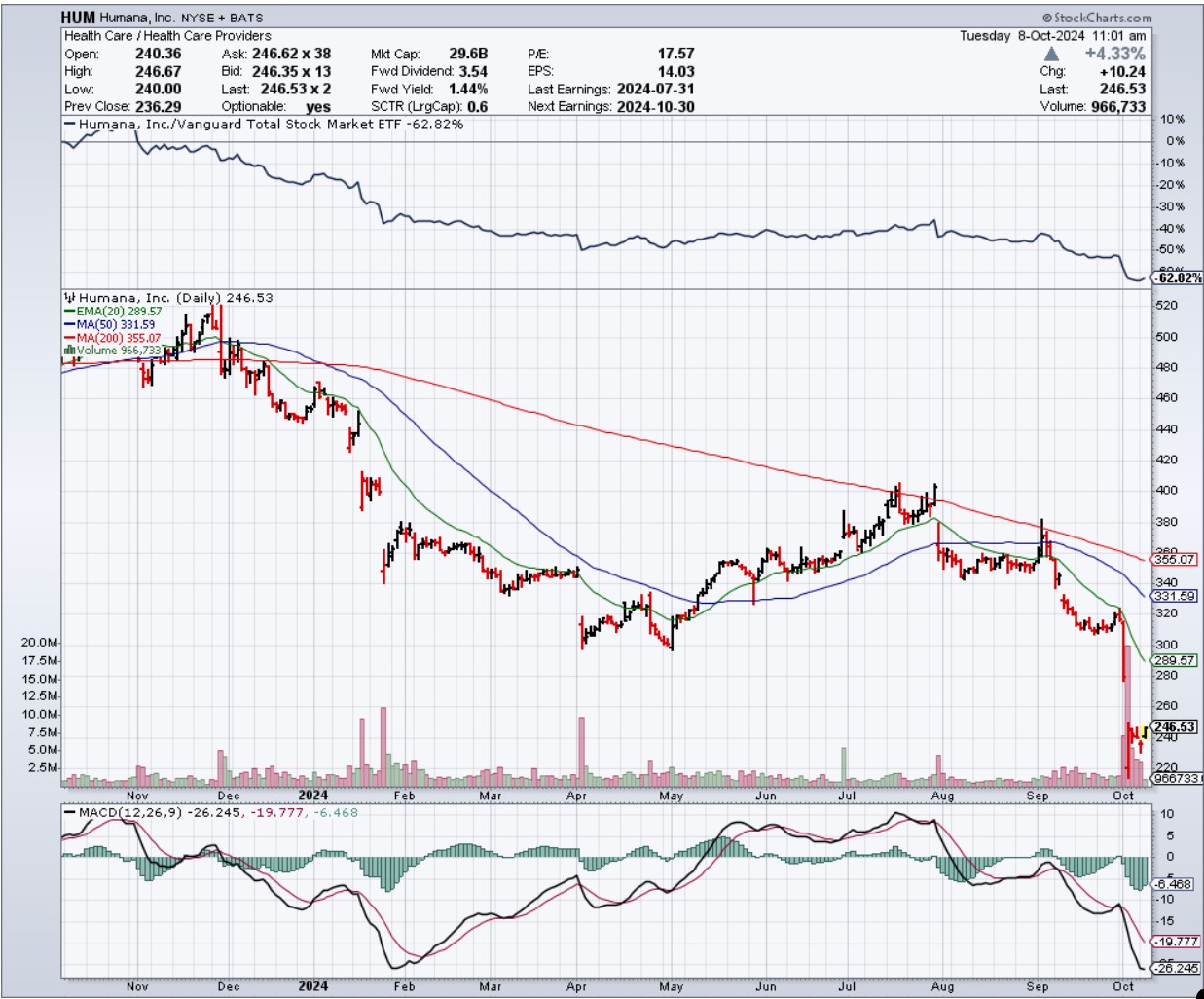

THE CHART SAYS….

Humana’s longer-term stock chart was already showing the need for a significant stock turnaround even before the CMS Starts rating cut. This chart (below) from StockCharts.com shows that HUM shares were unable to hold above the 200-day moving average in September and July and that the 200-day moving average will remains in a downward trend for some time even if its stock price recovers (it was a $520 stock a year ago!). Now HUM shares are about $100 lower than that 200-day moving average.

For the near-term chart action, HUM stock may be signaling some stabilization after the latest plunge. It has after all already lost half of its value from a year ago. HUM also bottomed out around $220 at the worst part of its plunge and the stock is back up to $245 at the present time. In no way is this meant to convey that a full recovery is on the way. But if there is a favorable appeal announcement as soon as October 10 or shortly thereafter, then HUM may be able recapture more of the losses from the $320 price before its most recent plunge.

Chart provided by StockCharts.com

Categories: Investing