CrowdStrike Holdings, Inc. (NASDAQ: CRWD) has gone from an obscure behind the scenes cybersecurity player to a household name during the summer of 2024. It wasn’t the great growth story. It wasn’t even that the company’s software was so widespread among large companies who were in turn serving millions upon millions of customers around the world. The reason CrowdStrike is now so well-known is because of its upgrade attempt that turned into a worldwide outage. The company’s software update truly caused chaos. That was then, and perhaps investors should be considering whether or not CrowdStrike will be a good fit in their own investment portfolios.

Most of the public might not even really understand what CrowdStrike does for its customers. It is a behind-the-scenes cybersecurity provider. The earnings report came in better than many investors had feared.

CrowdStrike’s shareholders probably had no idea just how much risk there was in a large service upgrade going awry prior to this outage. The software update was supposed to be routine. It wasn’t. Systems crashed. Clients had severe issues providing services. Airlines, restaurants, hotels, financial services, medical facilities, and so on.

FROM CRASH TO RECOVERY

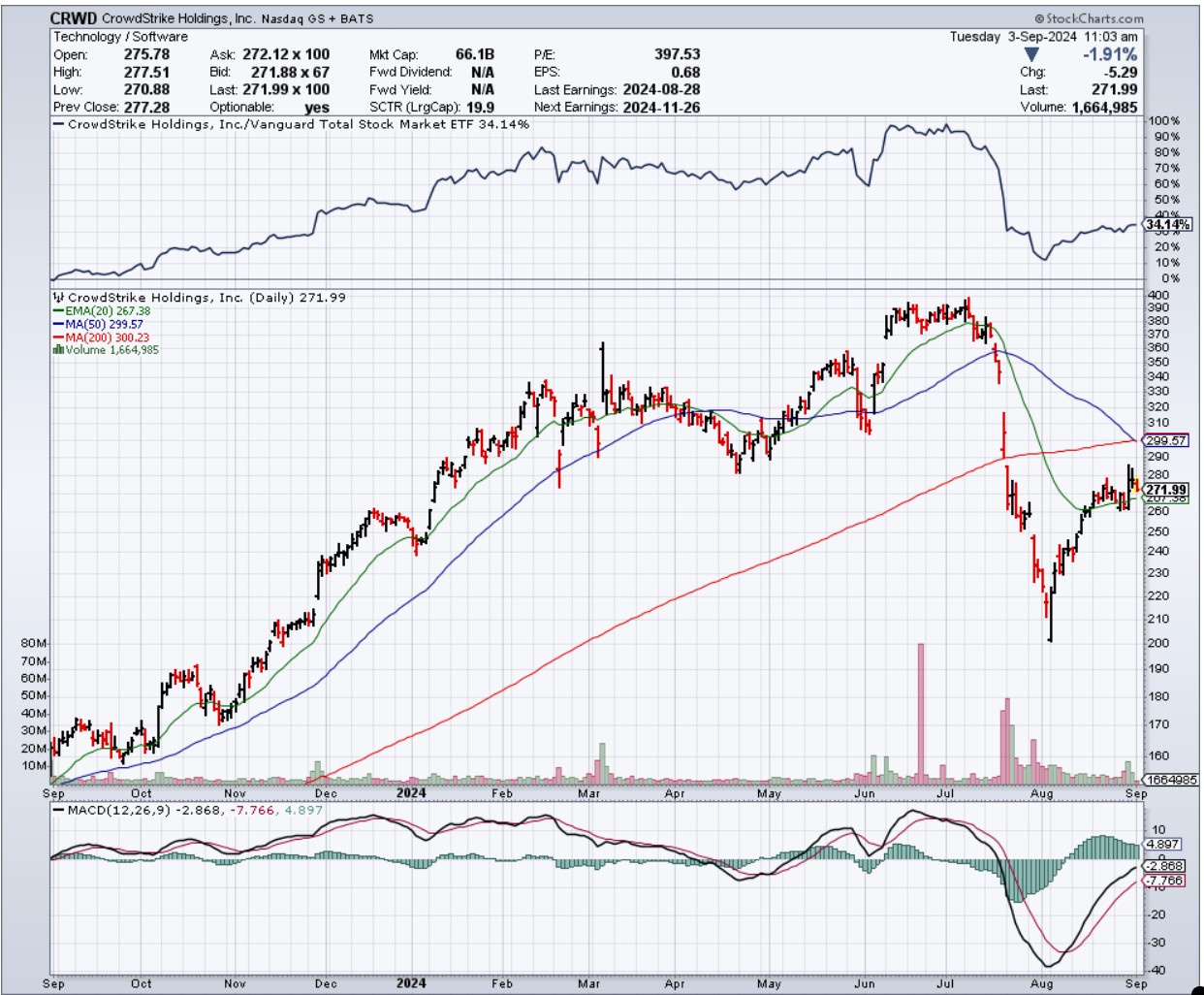

In just a few days the stock fell from $343 to $254… Then the stock market panic sell-off in Late-July and the start of August took the stock as low as $200 before normalizing at $230. And with a gradual recovery up to $265 before earnings, CrowdStrike’s stock closed out August at $277.28.

This in no way should imply that CrowdStrike a “screaming buy” for all types of investors. There can be no assurances that CrowdStrike’s woes are completely over and there are no assurances that its stock will rise. Some investors should probably avoid this scenario entirely due to above-average risks and a lack of dividends. This report is not intended to be used as investment advice. The decision to buy, sell, hold or avoid is up to each investor and should be made with a financial advisor.

THE POST-EARNINGS REACTION

The reaction after the earnings report during the last week of August may be interpreted as an all-clear sign to some more aggressive investors. Other investors are going to see the information and decide that much of the recovery has already happened. And we cannot ignore that September has historically been a weak month in market history.

Tactical Bulls is looking at CrowdStrike’s post-earnings analyst calls who are largely in defense of the stock, albeit with much more conservative price targets than before the outage. The stock’s chart should also offer some insight to long-term investors.

CrowdStrike’s guidance is said to have even considered customer compensation into the near-term expectations. And the outage is said to have driven only about $60 million in total deal delays pushing revenues out.

ONE BIG UPGRADE

One analyst formally upgraded CrowdStrike and raised its price target after the report:

HSBC raised CrowdStrike to Buy from Hold and raised its target to $339 from $302. HSBC’s quick take is that the financial impact of the July 19 SNAFU and outage is now known and the bad news is behind it. Despite lower guidance, HSBC noted that the guidance still implies strong revenue growth of 23% YOY for the next two quarters — nearly double the expected growth rates of other cybersecurity companies in HSBC’s coverage universe.

OTHER KEY POSITIVE REPORTS

We have seen some analysts stick with their pre-earnings price targets as well, although these may be lower than before CrowdStrike’s “incident” wrecked the stock. Here are two.

BofA Securities reiterated its Buy and maintained its $365 price objective. The firm gave several reasons to remain positive:

- Management showed the steps taken to ensure this doesn’t happen again;

- endpoints are one of the most strategic parts within cybersecurity defense, and CrowdStrike is one of the most effective solutions with no signs of market share loss;

- the expected impact on the nnARR (Net New Annual Recurring Revenue) was better than feared, at $30M each quarter versus $30M-$60M per quarter expected;

- and its new revenue growth guidance looks like it “de-risked” third and fourth quarter expectations.

Morgan Stanley reiterated its Overweight rating and its $325 price target as the second half is now “de-risked” and the focus is now shifted to the pace of topline recovery over the next 12 months to 18 months. The firm assumes 40-times its enterprise value over free cash flow and sees the post-outage recovery at $7.50 FCF in 2026, but calls it conservative and sees about $9 FCF/share in its bullish case.

Truist Securities reiterated its Buy rating with a $325 target.

THE ANALYST BRIGADE

Then there is a whole analyst brigade that maintained their (mostly positive) formal analyst ratings but still cut their price targets to more reasonable levels. Keep in mind that CrowdStrike recognizes more than 40 analysts with ratings on its stock. Here is the bulk of what was seen:

- Barclays reiterated its Overweight rating and raised its target to $295 from $285.

- BMO Capital Markets reiterated its Outperform rating and raised its target to $315 from $290.

- D.A. Davidson reiterated its Buy rating and raised its target to $310 from $290.

- Many analysts have still maintained positive ratings but they have had to drive their price targets lower. Here are the calls seen after earnings:

- Argus maintained its Buy rating but cut its target to $325 from $400.

- Canaccord Genuity maintained its Buy rating but cut its target to $330 from $340.

- Cantor Fitzgerald maintained its Overweight rating but cut its target to $350 from $400.

- Needham & Co. maintained its Buy rating but cut its target to $350 from $375.

- Oppenheimer maintained its Outperform rating but cut its target to $365 from $450.

- Raymond James maintained its Outperform rating but cut its target to $275 from $380.

- Rosenblatt maintained its Buy rating but cut its target to $325 from $330.

- RBC Capital Markets maintained its Outperform rating but cut its target to $335 from $345.

- R.W. Baird reiterated its Outperform rating but trimmed its target to $315 from $335.

- TD Cowen maintained its Buy rating but cut its target to $380 from $400.

- UBS maintained its Buy rating but cut its target to $310 from $330.

THE STOCK CHART

The following chart is courtesy of StockCharts.com.

Courtesy of StockCharts.com

AND FINALLY…

CrowdStrike closed out August at $277.28, up from $231.96 a month earlier but still down handily from the $350 share price before its outage. It was trading at $271.50 on the first trading day of September. Its 200-day moving average was $299.57 as of the start of September.

Categories: Investing