Argentina is an economy that experiences its ups and downs in ways that are unimaginable to the United States. Hyperinflation, complete economic shifts, and those might not even be the biggest challenges. Argentine president Javier Milei has delivered on his economic reforms, but there have been some significant rough patches along the way.

Tactical investors are willing to place their capital wherever they believe it will be treated the best. Safety in times of turmoil and outsized gains in times of plenty. Now is the time for tactical investors to consider if other emerging markets (like Argentina) might offer better upside than the U.S. ahead. The outcome of that thought process will depend on many factors, and the main data below comes from “Argentina’s Unexpected Turn” from BofA’s Latin American research team.

The local Merval exchange had rallied 16% in this last week alone on word that the U.S. Treasury may offer support. And according to BofA Securities, Latin America saw another $200 million in inflows into equities this week in emerging market investors — for a total YTD inflow from global funds of global funds dedicated to Latin America of $2.8 billion.

One issue that was brought up by BofA’s global team is that a “financial bazooka” and a new safety net may be headed to Argentina if the U.S. Treasury offers material support to Milei’s recovery plans. This may even mean that foreign exchange intervention is now less likely — and perhaps that there is now a new potential lender of last resort.

As for whether or not the worst is over, BofA’s global research team sees that the “negative case scenario” for Argentina is already priced into the markets. This is a time when the Merval is down 45% YTD, versus a gain of about 13% for the S&P 500 in the United States.

Argentine has faced another credibility crisis that weighed on equities and the currency. According to BofA’s team:

We think a more challenging scenario is likely already priced and we remain overweight Argentina in our portfolio through energy and banks … Despite incorporating macro headwinds, our financials team expects 2026-2027 earnings rebound for Argentine banks.

Now the wild card comes from the upcoming election in Argentina on October 26. BofA sees it as a make or break moment — The mid-term election outcome will be key for governability and continuation of prudent policies, and potential structural reforms (privatization, tax system overhaul to increase efficiency, labor reform, a social security reform proposal).

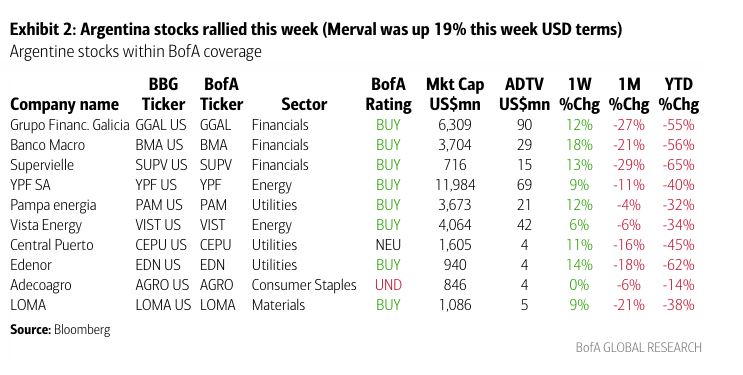

A table in the image below shows BofA’s tracking of key Argentinian stocks.

source BofA Securities

Global X MSCI Argentina ETF (ARGT) had peaked at $95 earlier in 2025. It was down 1.6% on Friday to close at $72.92. Again, the US S&P 500 is up about 13% YTD and this Argentine ETF is down about 12% YTD.

The verdict for 2026 is still to be determined.

Categories: Economy, Investing, Personal Finance