Micron Technology, Inc. (NASDAQ: MU) has once again acted as a preview for what to expect from major semiconductor companies in their earnings reports coming out over the next month. Micron’s quarter was one of record revenues — at $11.3 billion, up 46% from last year! The driving is force now is strong demand for AI products and High Bandwidth Memory rather than just basic NAND/DRAM demand for PCs and other consumer electronics.

Where things get tricky is that Micron’s stock was already up over 90% YTD ahead of the earnings report. And now its commentary about the state of the chip industry and economic uncertainty are in the way.

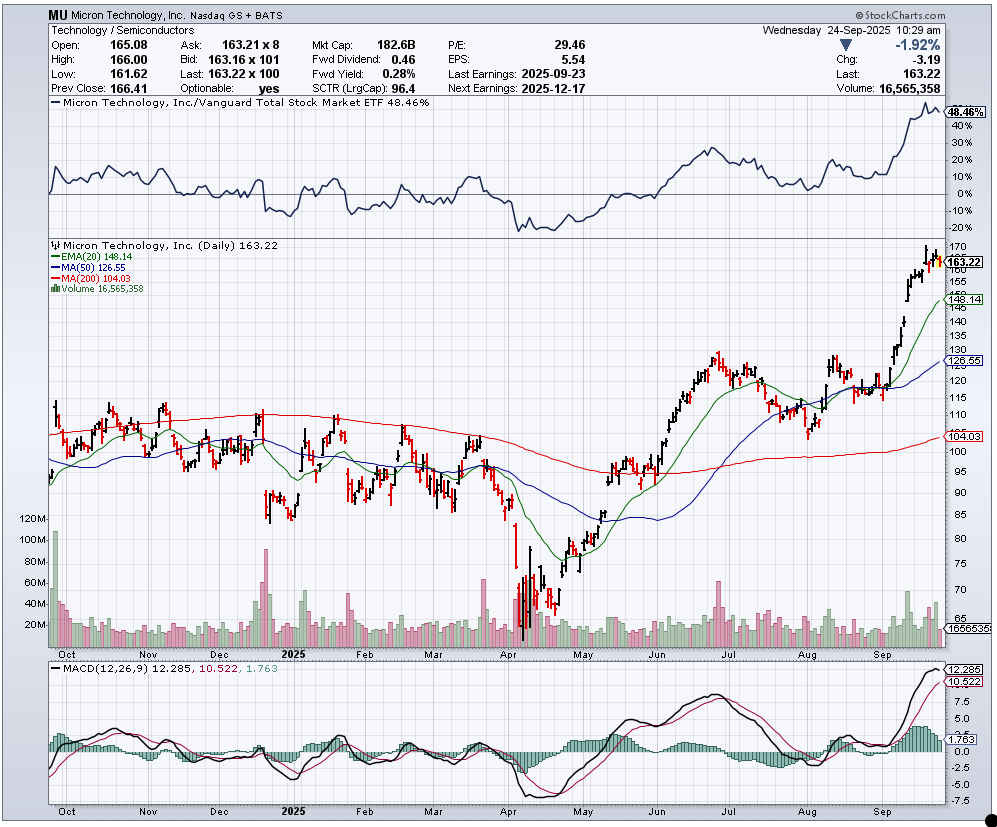

Micron’s next-day initial reaction was down 1.9% at $163.20 after an hour of trading. It had also seen almost a full day’s worth of trading volume (20 million shares) just after the first hour -plus over 10 million shares in the after-hours reaction the evening of earnings!

Micron’s guidance for next quarter ($3.41-$3.71 EPS and $12.2-$12.8 billion in revenue) are against consensus estimates of $3.73 EPS and $12.5 billion in revenue. It is good guidance, but investors need to consider that gains of nearly 40% in the last month and over 90% in 2025 (YTD) may have priced in some of that good news.

Tactical Bulls wants to see what Wall Street’s top analysts are telling their clients what to. Most of the comments are coming with reiterated ratings and higher price targets. Much higher price targets in some cases.

Investors are going to have to get over the fact that what used to never be worth more than 8-10 times earnings is a much different story now. AI and High Bandwidth Memory have changed the narrative, and there is still the next wave of demand from smartphones, PCs, tablets and peripherals all lined up to drive higher earnings and stronger margins.

Please note that all analyst ratings and price targets below have been sourced to each brokerage firm listed by name. Tactical Bulls does not maintain any set price target or formal rating of its own on Micron. These are the top analyst calls for Micron after earnings on the morning of September 24, 2025.

Barclays reiterated its Overweight rating and raised its price target to $195 from $175.

BofA Securities maintained a Neutral rating, but the firm still hiked its price objective to $180 from $140. While BofA did also raise its own sales/earnings/margin estimates it believes much is priced into the stock after 90%+ gains YTD.

Cantor Fitzgerald reiterated its Overweight rating and raised its target to $200 from $185.

ALSO READ: 15 ANALYST STOCKS TO SELL NOW!

Citigroup reiterated its Buy rating and raised its target to $200 from $175. Strong AI demand, better pricing, a tightening DRAM market in 2026 and upside in demand are all cited.

JPMorgan reiterated its Overweight rating and the price target was hiked to $220 from $185, noting strong data center sales, firm to higher price trend and a favorable setup through 2026.

KeyBanc Capital markets reiterated its Overweight rating and it raised its price target to $215 from $160. While the report was dominated by strong DRAM pricing, order flow at set prices for 2026 are going to drive higher margins.

Mizuho reiterated its Outperform rating on Micron and the firm hiked its price target to $195 from $182 in its call for higher earnings, revenues and margin.

Morgan Stanley maintained its Equal-Weight rating with a $160 price target, noting that after such strong gains Micron could still see some margin headwinds in High Bandwidth Memory.

Needham & Co. reiterated its Buy rating and hiked its target to $200 from $150. Gross margin expansion for 2026 are backed by higher prices, a favorable revenue mix and cost cuts are the driver on top of higher guidance.

Piper Sandler reiterated its Overweight rating and it raised the target to $200 from $165. Higher margins and being sold out of its 2026 High Bandwidth Memory capacity in the coming months were behind the call.

Raymond James reiterated its Outperform rating and hiked its target to $190 from $150.

Rosenblatt reiterated its Buy rating and has moved from above-consensus to handily-above-consensus with its former $200 target being hiked up to $250. Higher-margin products, raising prices, cost cutting and higher demand from all of its end markets are the catalysts for an even higher price target.

ALSO READ: THE COMING FLOOD OF ALT-COIN ETFS!

Stifel reiterated its Buy rating and raised Micron’s price target to $195 from $173. This targets higher margins from Micron’s cloud and hyperscale memory segment as a structural shift in revenues.

UBS reiterated its Buy rating and raised its target to $195 from $185.

Wedbush Securities reiterated its Outperform rating and raised its target to $220 from $200 in the call.

Wells Fargo reiterated its Overweight rating and raised its target to $220 from $170. The is now targeting a path for $16-$18 per share in earnings.

A one-year chart courtesy of StockCharts.com has been provided below.

Categories: Investing