![]()

Unisys Corporation (NYSE: UIS) is one of the old-school information technology providers that many investors have completely forgotten about. It came public in 1981 and it’s just a company (and stock) that you never hear about any more. Unisys’ market cap is a mere $275 million, and its prior $3.82 share price was less than half of its high in the last year — and don’t overlook that Unisys was a $35 stock ten years ago and the company has shrunk handily over time.

Now, it may be the case that Unisys is back as a potential under-the-radar tactical investment for speculative investors who are willing to roll the dice on an IT services turnaround stock that time has left behind.

Tactical Bulls is taking a deeper dive into what may be the big attraction here, with a warning that $UIS has been such a long-term disappointment to investors that there are likely many skeptics wondering if a turnround like this is even possible after this long. This turnaround may not be for those investors who are risk-averse or want solid operating histories and a track record of dividends and gains.

It seems possible that Unisys could be sitting on an “ace in the hole” with the cloud and artificial intelligence that may not be priced into the stock. And there feels like a light at the end of the tunnel covering its underfunded pension obligations from the past that may feel at least a but similar to the perpetual U.S. Postal Service’s pension woes.

EARNINGS, AI, TRENDS, OPPORTUNITIES…

Many other down and out IT and tech companies have seen their stocks rally handily from the potential upside of their AI and cloud efforts. That hasn’t happened for Unisys yet (and it may not happen). Here is what Unisys CEO & President Michael Thomson said about that opportunity:

The investments we made in applying agentic and generative artificial intelligence capabilities to our most innovative solutions are beginning to advance our growth and efficiency priorities as evidenced by our improved profitability and enhanced cash generation.

And more recently, Unisys outlined Agentic AI opportunities for it and peers. The company’s findings showed that 78% of organizations are planning to increase investment in genAI, and 73% of business executives now see agentic AI as critical to staying competitive. The opportunity for growth — only 36% of those organizations say that they are ready to support large-scale AI workloads.

Unisys posted a positive upside on its latest earnings report, and there may even be a good old fashion upside pending from its longstanding pension obligations.

Two analyst reports have highlighted significant upside potential for Unisys. While Tactical Bulls always reminds readers that no analyst report should ever be the sole reason to buy or sell a stock, what stood out was that the implied upside ranged from 55% to over 100% if those analyst price targets come to pass.

There needs to be another warning, particularly for such a risky stock like Unisys. No analyst reports with Buy ratings and huge upside price targets are ever issued with any assurances that even any of that huge implied upside will be seen. Investors and traders should also know that there are no such things as “money-back guarantees” issued with any analyst reports either.

BIG EARNINGS, WITH CAVEATS…

When Unisys reported earnings in August, it was shown to be “strong sequential improvement” in revenue and profitability… and Unisys also confirmed it was taking strategic steps to mitigate its U.S. pension volatility. Its stock even rose 8% at the time because of sequential revenue growth, stronger profitability metrics and due to a strategic financial restructuring.

Reported revenues of $483.3 million were nearly $40 million (10%) higher than expected. This represented a 1.1% annualized revenue boost, but it was sequential revenue growth of 11.8%. The company tied this to higher license/support sales aided by the timing of software renewals and also by stronger support subscriptions.

Unisys was also back to being in the black on an operational basis with non-GAAP earnings of $0.19 EPS (versus an expected loss on EPS) and better than $0.16 EPS for the same quarter a year earlier. The company did indicate that its gross margin dropped slightly, down to 26.9% from 27.2%, because of higher-cost reduction charges.

Unisys had also narrowed its 2025 revenue guidance (in constant-currency) and even managed to raise its non-GAAP operating profit margin guidance. The company showed that its backlog of orders on the books but not yet completed was $2.92 billion — up from $2.79 billion at the end of Q2-2024. That backlog was $3.0 billion at the end of 2023.

A full review of Unisys earnings report and SEC filing will outline some additional data on trends. Some of those figures and trends were less positive than the headline data.

CLEARING THAT PENSION DECK

Unisys is not a small company despite serious headcount reductions over time. Its latest annual report (2024) showed that the company employed approximately 15,900 professionals across the globe at the end of 2024. Of those, 2,500 were U.S. based and 13,400 were located in other countries. Still, that headcount shows a significant drop over the long haul — it had 36,900 employees at the end of 2000 and 23,200 employees at the end of 2014.

And what about reducing that ongoing pension obligation that has been a thorn in Unisys’ side for years? The 2024 annual report did confirm it was an underfunded pension plan. As of the end of 2024, Unisys had an estimate of approximately $750 million in aggregate from 2027 through 2034 (beyond current and 2026 obligations). The company’s press release as of the late-July earnings report said:

The company significantly reduced future cash contribution volatility within its U.S. qualified defined benefit pension plans following changes to its pension asset investment strategy and a discretionary contribution of $250 million… The discretionary contribution was funded using a combination of $50 million cash on hand and $200 million of proceeds from the company’s issuance of $700 million senior secured notes due 2031, with the remaining proceeds used to refinance the existing $485 million senior secured notes due 2027.

Unisys also said that its capital structure transformation has removed “substantially all volatility” from its U.S. pension contributions and that it has established a more defined path to fully removing its U.S. pension obligations. The timing of that “fully removing” was not defined its release

WALL STREET’S BIG BOLD TARGETS

Needham & Company issued a new Buy rating and a $6 price target on September 3. While the firm noted Unisys is a global IT-solutions provider covering a broad list of industries, the report highlighted several issues:

- Cyclical pressures have weighed on industry growth,

- it should return to growth as the operating environment improves

- it can continue to expand its margins,

- it can remove the overhang of its U.S. pension plan within 5 years,

- and (perhaps most importantly) is the call that its stock can re-rate higher as that pension overhang begins to disappear.

Back on August 4, Maxim Group raised its rating on Unisys to Buy from Hold and the firm set an even more aggressive $9 price target for the 12 months ahead. This was more than a “double your money” forecast if its thesis pans out. The firm pointed out that its $0.19 earnings per share was handily above expectations.

And even earlier in February-2025, Canaccord Genuity maintained its Hold rating on Unisys while cutting its price target to $6.50 from $7.00 at that time. Unisys shares were trading down at $5.09 — after having been at $5.94 the prior day and even higher at $6.69 just two days earlier.

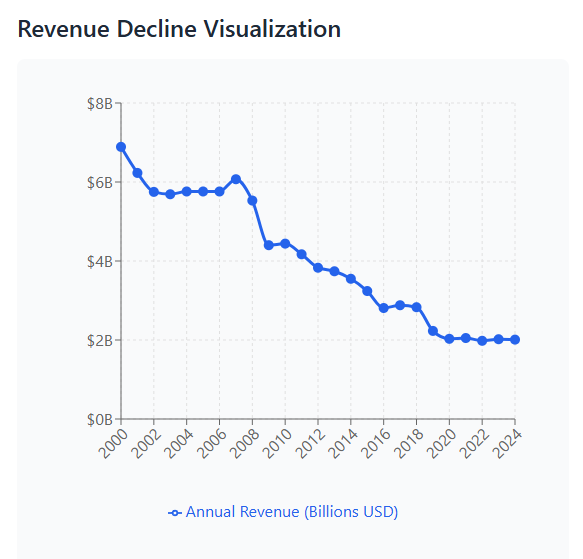

AI-ASSIST: HUGE REVENUE DECLINE

Tactical Bulls used Anthropic’s CLAUDE to draw a visualization of just how much Unisys has declined in annual revenues over time. This actually goes back to the year 2000 to show that representation visually. And in case there are any concerns over what it really says… Yes, this went from generating over $6 billion in annual revenues 25 years ago and it represents only about $2 billion annually now. Then again, if that turnaround and growth strategy works then maybe there are good trends ahead to win from.

Claude shows BIG GIANT revenue decline over the decades…

THE RESPONSE & STOCK BASICS

Unisys also has a heavy institutional ownership and its short interest of 1.92 million shares represents only 2.7 days to cover based on average daily trading volume of about 730,000 shares. Unisys shares also have a 52-week trading of $3.56 to $8.93.

Its stock was up only about 1% at $3.86 on Wednesday with about 175,000 shares having traded hands after about an hour of the normal trading day.

DISCLAIMERS & WARNINGS

The analyst ratings and price targets referenced above have been credited to each firm by name. Investors should keep in mind that analysts sometimes get their thesis and outlook wrong, which can result in potentially large losses for investors. Market fundamentals and company fundamentals can also change from positive to negative in an instant.

Tactical Bulls does not maintain any formal ratings and nor does it maintain any price targets of its own regarding Unisys and other competitors that may have been mentioned in this reporting. Interpretations of how positive or negative the analyst calls are can also wildly vary from investor to investor. Some investors will even use every bit of good news to sells shares (or short sell).

And a final reminder, again… No analyst ratings and their price targets, even those with the strongest conviction or strongest pessimism, ever come with any guarantees of profits. Analyst reports also never have money-back guarantees in the event that investors lose money.

Categories: Investing